There's no wrong or right way to budget, but finding a method that fits your unique money situation can make all the difference in helping you reach your financial goals. YNAB, short for “You Need a Budget,” is a fantastic tool that can help you reach your cash flow goals more efficiently, faster, and—may I say—with less agony and frustration. In this YNAB review, we're excited to share how it can help you finally get a firm grasp on your cash flow.

Who is YNAB?

While there are many available budgeting programs, none are quite like YNAB. Not only does it aim to help you track the inflows and outflows that make up your budget, but it also provides you with an entire framework for how to view spending and saving. After all, success with money is said to be 80% behavior-related and only 20% attributable to knowledge.

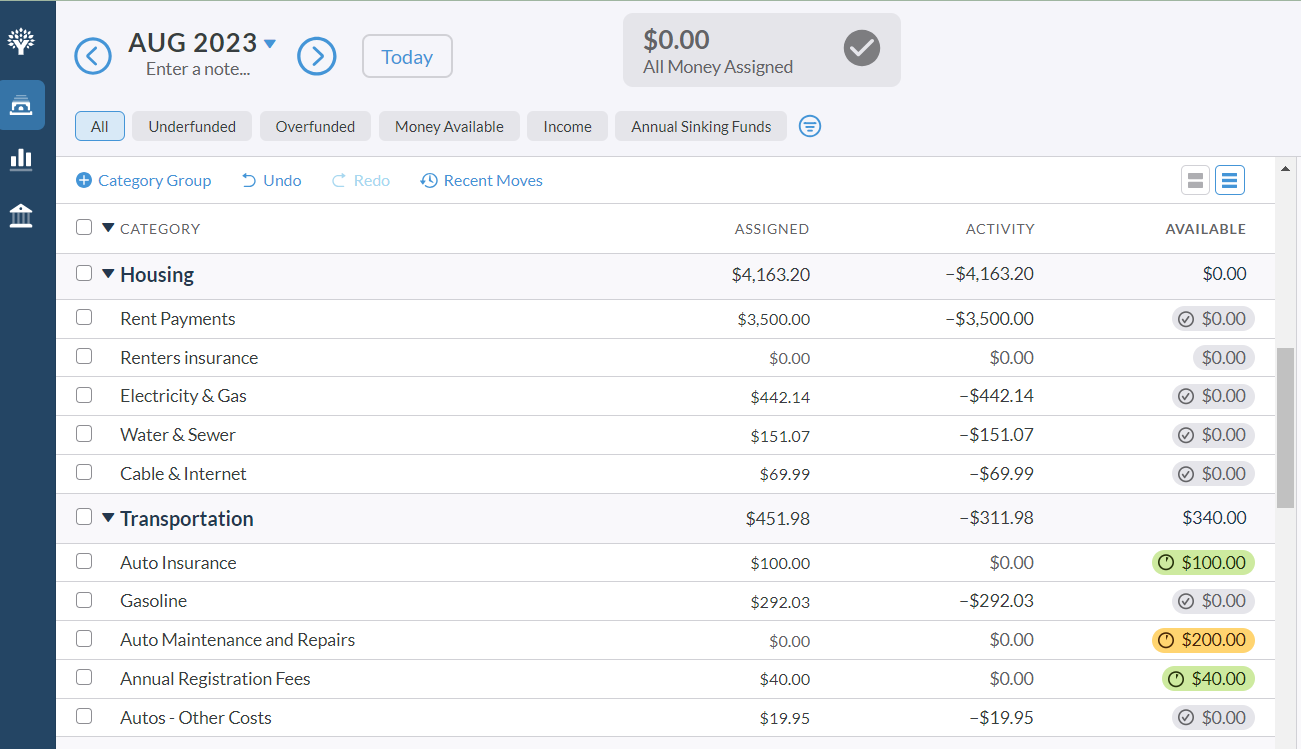

YNAB originally started as a spreadsheet, which won't surprise you when you look at even the most current iteration of the software. Its clean interface identifies your budgeted, spent, and remaining amounts (or, in YNAB lingo: assigned, activity, and available balances).

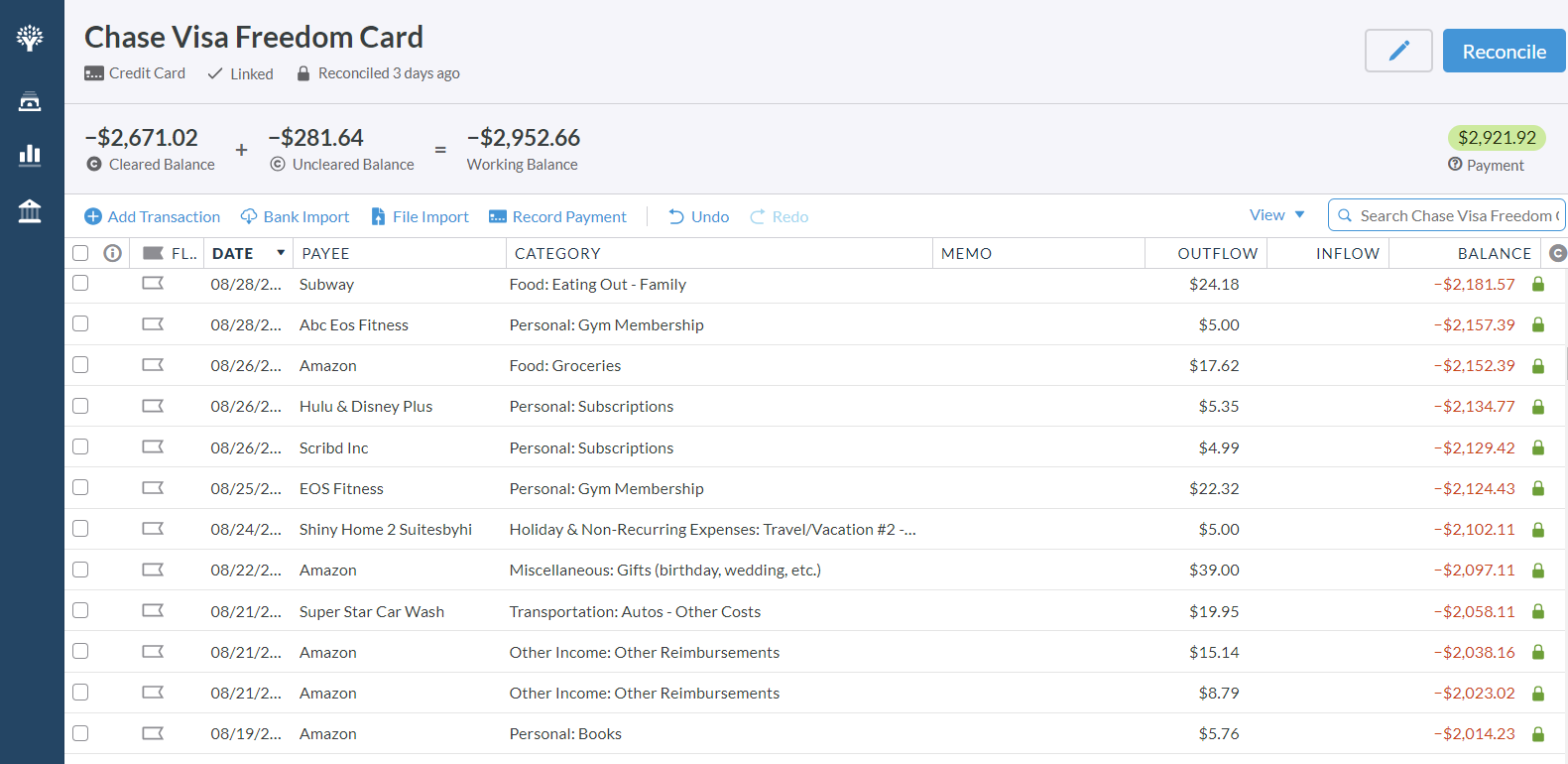

The transaction side of YNAB is reminiscent of an old-style check register (I'm dating myself here for sure!), showing a listing of transactions by account, date, payee, amount, category, and other additional notes.

And with such a straightforward name like “You Need a Budget,” you won't be surprised that an accountant started it (see Andy's interview with Jesse Mecham here!).

In addition to its core budgeting software, YNAB is heavily focused on providing financial education to its users.

YNAB is currently available for the Web, iPhone, Android, iPad, Apple Watch and Alexa.

How Do You Use YNAB?

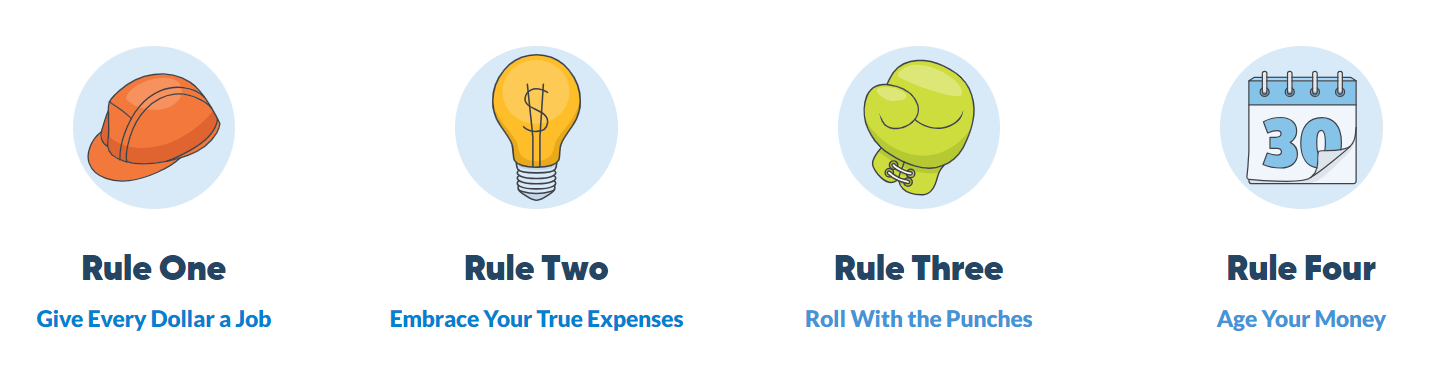

A discussion of YNAB wouldn't be complete without a brief discussion of their 4 “rules.” Not only are these rules, but they are also the steps you take to complete a budget in YNAB.

Rule One: Give Every Dollar a Job

After adding your financial accounts, the first thing you do in YNAB is assign all of the money you currently have to categories (referred to in this rule as “jobs” that you want your money to do). Note that you're not strictly assigning your income but every single dollar you have in your bank accounts right now.

This process is similar to zero-based budgeting but goes a step further by including all your available funds, not just your income.

Rule Two: Embrace Your True Expenses

With the YNAB method, you'll never be “surprised” by annual car registration fees, subscriptions, repairs, or even Christmas (um, yes, this does indeed happen every year, so it definitely shouldn't be a surprise expense).

Setting targets and saving monthly for these expenses means the money is there—both in your account and your categories—when you need it.

Rule Three: Roll with the Punches

The biggest reason (by far!) that people give up on their budget is because they struggle with overspending. No one wants to feel like a failure, and that's where the flexibility of YNAB comes in.

Not only will you gain clarity about how much you spend, but you can also simply change your budget throughout the month. Spent too much on eating out this month? Throw some money at the problem and move money around from another category to cover it. You'll likely think twice the next time you’re tempted to take funds from your “Travel to Europe” category.

Rule Four: Age Your Money

The three rules above focus more on the logistics of creating your YNAB budget. However, this last one is more of a goal to reach than a step to complete. “Aging” your money is simply another way of describing getting out of the paycheck-to-paycheck cycle and creating an emergency reserve.

It’s as simple as this: the longer your money has been sitting in your accounts without being spent, the greater your age of money. This is a tangible representation of your financial progress.

While requiring more hands-on engagement than other budgeting software programs, following the four rules helps maximize your intentionality around your finances and minimize financial stress.

YNAB Review: Best Features

Over the years, YNAB has gradually expanded from a zero-based budgeting spreadsheet to a full-featured budgeting software program that manages all cash-flow aspects of your financial life, from budgeting to debt repayment.

Here are some of the top things people love about using YNAB:

Efficient (But Still Intentional) Money Management

YNAB helps you to optimize the time you spend regularly managing your budget. It strikes a balance between allowing you to automate the import and categorization of your income and expenses (a tedious, generally non-value-added task) and requiring you to actively approve each transaction and move money from other categories when you've overspent. This ensures that you are being intentional and aware of your spending.

In addition, the focus on saving in advance for future “true” expenses by setting monthly target amounts helps minimize financial stress.

The mobile app makes it easy to track and monitor spending on the go so that you always have up-to-date information about how much money you have left in each category.

Ability to Customize

One of the most loved features of YNAB is the ability to customize nearly every aspect of your budget, including:

- Account names and order in which the accounts are shown

- Category groups and subcategories and their listed order

- Scheduled transactions (which link seamlessly to any transactions subsequently imported in)

- Off-budget accounts (known in YNAB as tracking accounts) that factor into your net worth but are not included in your budget (such as brokerage and retirement accounts, mortgages, etc.).

- Debt payment strategies, including analyzing the impact of making additional principal payments toward your debt

Customizations in your YNAB account allow for more clarity in your financial situation and better insight into how you can reach your important goals.

Collaboration

The “YNAB Together” feature allows you to share budgets with your partner, financial coach, or your kids. You can manage which specific budgets you would like to share and with whom while keeping other information private. Up to 5 collaborators are allowed without an additional subscription fee.

Education & Support

From the minute you sign up for a YNAB account, you are given step-by-step prompts to help you set up your accounts, categories, and targets (targets are essentially your financial goals).

Need more help? You have options:

- Attend one of the many live onboarding sessions

- Watch tutorial videos (check out Hannah's YouTube videos–she's so fun!)

- Read the YNAB book to learn more about the system behind the software

- Join the active YNAB Facebook group

- Check out the YNAB-certified coach directory

No Pesky Advertisements, Upsells, or Advisor Calls

YNAB receives revenue solely from paid subscriptions and has no advertisements, premium subscription tiers, or other products. While they have a directory of YNAB coaches, they do not receive any related compensation. Also, you'll never receive unsolicited calls about services.

You will, however, receive loads of emails to help you get started, but those are easy enough to opt out of if you don't wish to receive them.

YNAB Review: Areas for Improvement

Somewhat Steep Learning Curve

Due to the different mindsets required when using YNAB versus other more simplified budget programs, there is a significantly steeper learning curve to learning the software.

Understanding how credit cards are treated in YNAB often presents challenges for new users, as money spent using credit cards essentially offsets other available bank balances.

Taking advantage of live webinars and researching YNAB's help directory can help you quickly find answers to your questions. Once you’ve used it for a few months, you will fully understand the process and how everything ties together.

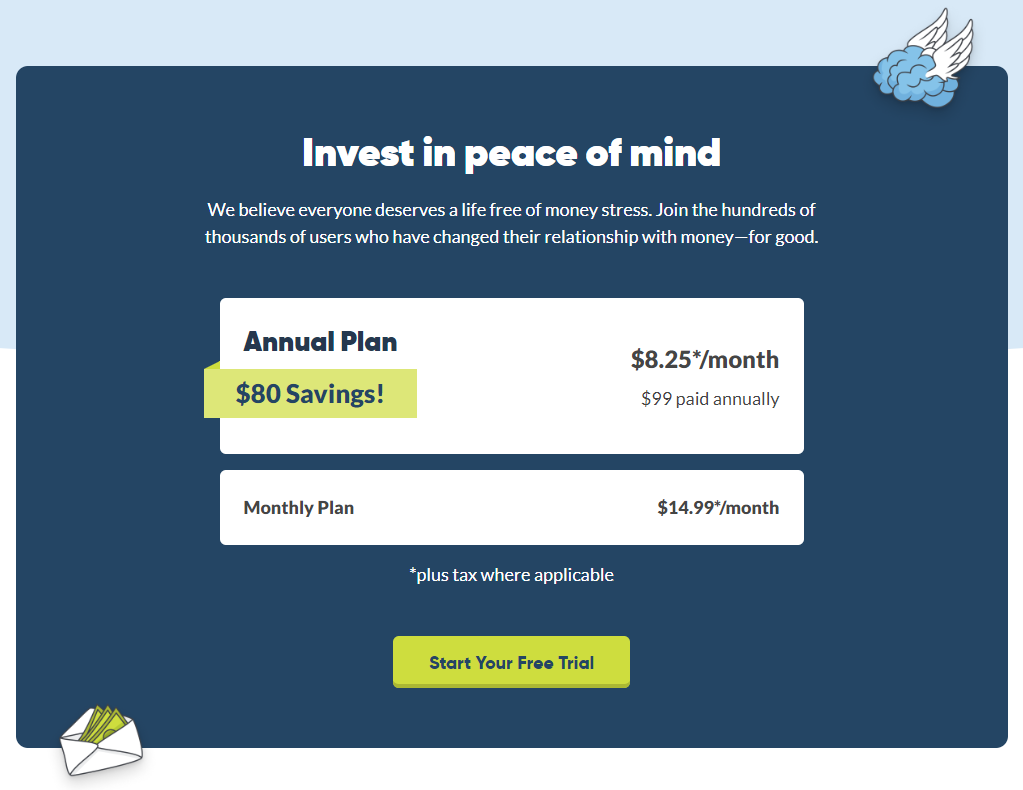

Cost

Unlike other budgeting tools such as Mint or Empower, YNAB is not free to use. A subscription to YNAB will cost you $14.99/month if paid monthly or $99/year if you pay upfront.

The increased awareness, however, results in the average new user saving $600 in the first two months and $6,000 in the first year, according to YNAB. Overspenders could easily earn back the $99 subscription fee in credit card interest savings alone!

There is a free 34-day trial (no credit card required) to see if YNAB will work for you.

Not A Full-Service Money Application

YNAB is not a one-stop shop when it comes to complete money management. It does not include detailed investment tracking, credit monitoring, bill-tracking, or bill-paying features. If these things are important to you, it will be necessary to use other tools in addition to YNAB.

Limited Reports

One of the biggest complaints from YNAB users is that reports are somewhat limited. Additionally, the reports are not currently available on the mobile app. The basic net worth and cash flow reports are customizable by date, accounts, and categories.

Those who want more granular data can export accounts, budgets, and transactions to a CSV file, where they can further analyze their data.

YNAB Competitors

Focusing on being intentional with your money before it's spent rather than simply tracking what you’ve already spent is the main differentiating factor from other budgeting software programs.

YNAB vs. EveryDollar

EveryDollar is a top YNAB competitor. So how does EveryDollar bring the heat? Through Dave Ramsey, of course!

Many people discover the world of personal finance as a result of Dave Ramsey. Whether they have already completed his Baby Steps program or are still working through it, many people connect with his budgeting platform called EveryDollar.

EveryDollar is a budgeting tool and spending tracker. You can build your money goals into the app. Then, EveryDollar will help you strategize ways to pay down your debt. The app also integrates the Baby Steps, so people who currently use that program will find this tool to be a logical pairing.

However, it is worth noting that EveryDollar doesn't track your investments. If that matters to you, you will definitely want to consider other budgeting tools.

YNAB vs. Monarch Money

Monarch Money is another paid money management program at the same price point as YNAB that offers many of the same features:

- Automatic bank importing

- Ability to share your finances with a partner

- A focus on reaching financial goals

In addition, Monarch Money also allows you to track your investments in more detail. This allows you to customize how you view your information in their dashboard.

If you're looking for something more focused on intentional budgeting and don't want or need the additional information Monarch Money provides, YNAB will be a better fit.

For more details, check out our in-depth YNAB vs. Monarch showdown!

YNAB vs. Empower

Most people in the personal finance community are already familiar with Empower (previously branded as Personal Capital). Not only do they have robust budget tracking features, but also investment tracking and fee analysis, retirement planning, and more. However, you can expect to receive a sales phone call if you've linked more than $100k in assets.

If you want to keep your data private, avoid advertisements and sales pitches, you'll likely prefer YNAB.

We also dive deeper into all things YNAB vs. Empower here!

YNAB FAQ

How much does YNAB cost?

YNAB is subscription-based at $14.99/month or $99/year for upfront annual payments. You can sign up for a 34-day free trial with YNAB without entering any payment information.

College students are eligible for a free one-year subscription by emailing YNAB support with proof of enrollment.

Who does YNAB work best for?

YNAB is best for those who want to optimize their finances, create a zero-based budget, or are struggling to break the paycheck-to-paycheck cycle. It requires someone willing to learn a new method of managing their money.

Is YNAB safe?

Yes! YNAB is safe. YNAB takes your security seriously. So seriously, in fact, that their Security page is one of the most comprehensive plans we've come across in the fintech world.

They use bank-grade or better encryption. That means that your browser has to be encrypted when sharing your data. Additionally, as you use YNAB, they have a new browser security features that makes some kinds of data attacks against YNAB impossible.

If you do have concerns, you can reach out to their Security team at security@ynab.com.

Does YNAB work for couples?

Sure does! YNAB absolutely works for couples. Why? Because YNAB believes that couples should manage their money as a team. In addition to offering a ton of resources on how to address your finances together, YNAB has features built into the platform to help you do so.

One of the most important things you should know is that you can share your YNAB subscription with a partner for no extra cost! Though your subscription is shared, you each have your own log-in account. Plus, you can customize how to share spending plans and other information. Because YNAB knows that you want a team plan for your money, but not every account or spending plan might be joint.

Is YNAB good for a business budget?

You can use YNAB to build a budget for your small business! YNAB is best for businesses that don't have a ton of inventory or need to manage payroll for their employees. If you run a simple business, YNAB can absolutely work for you. The best part is that if you use YNAB to manage your personal finances, you will already have a basic understanding of how the platform is set up when you build a business budget.

Final Thoughts on our YNAB Review

If you feel like you're not spending intentionally as you'd like, YNAB may be the tool you need. This can help you both save more and spend more, albeit on the things that matter the most to you. Check it out with their free 34-day trial and see whether you become yet another YNAB super-fan who can't imagine their money life without it.

What do you think of this YNAB review? What has your experience been with YNAB?

Please let us know in the comments below.