You've heard about financial independence (or FIRE). The personal freedom, new options, and a relaxed lifestyle all sound amazing, but you don't know where to start. It's time to create a financial independence plan.

Just like any other major goals in life, you need to develop a pathway to get there. Graduating from college, landing your first career, and even finding your partner all took focused attention and clear direction. Financial independence is no different.

Once that pathway is laid out though, achieving your big goals becomes much easier. And when you arrive at your desired destination, you'll remember why you worked so hard to get there. The victory will be that much sweeter!

Let's do this!

Define What Financial Independence Means to You

There are many varying definitions of financial independence and, in a sense, I believe they are all correct. You know why? Because everyone's situation is unique. What “independence” means to one person may be completely different from another.

My financial independence plan may mean having enough in my savings account to take a chance on an entrepreneurial venture. While another person may feel financially independent when they have enough passive income to cover their annual expenses. It's all personal … that's why they call it “personal finance”!

Here are some different stages to consider as you are defining your financial independence plan.

A Comfortable Emergency Fund

When you have 3-6 months of expenses in the bank, as recommended by many financial experts, you can cover yourself for everyday emergencies and even job loss. This money in the bank has a way of not only improving your financial health but your mental health as well. Knowing you're protected (and that you're protecting your family) from the financial trip hazards of life can help you feel calmer and less stressed.

When you have an Emergency Fund, you're also helping yourself to stay out of any further debt. Instead of paying interest to the bank or credit card company, you can earn interest as you shield your money in a high yield savings account.

Debt Free

In this stage, you have no consumer debt in your life anymore. No credit cards, no student loans and not even a car loan. Life feels good when you're driving a paid for car!

When debt is eliminated from your life, you can use more of your money for fun, travel and investing for the future.

Mortgage Free

One of my personal favorite financial milestones is becoming mortgage free. With housing being one of the largest expenses in a family's budget, eliminating your mortgage forever can have a life-long positive impact on your family for generations to come.

Our family paid off our mortgage in 5 years and since then, we've been able to design our lives according to more of what we WANT to do instead of what we HAVE to do.

Coast FIRE

We've been told forever that we need to keep saving for our retirement. The more the better. At what point can we take a break and let compound interest do its magic? That's what Coast FIRE is all about.

For example, let's say you have $500,000 saved for retirement by age 40 and you spend around $60,000 per year. If you continue to invest that $500,000 in the stock market and earn a conservative 5% return and don't put another dime in your account, you could expect to have $1,693,177.47 in your account at age 65.

With a 4% safe withdrawal rate, you could easily live on around $67,000 per year. And that doesn't include any social security (who knows where it'll be in a few decades). Intriguing, eh?

Now everyone's situation is different and depending on how your retirement funds are invested, you may have to pay taxes in your retirement years on the investment income. Be sure to work with a certified financial professional (because I am definitely not one) on this concept and any other investment or retirement plans.

Millionaire Status

This stage is as straight forward as it comes. When you've increased your net worth to $1,000,000, you are officially a millionaire!

Now, in the end, this is just a number, but when you peel back the layers of what your net worth is made up of … that's when you feel the real financial independence. Perhaps no debt, no mortgage, income-producing assets, and healthy retirement savings. Talk about less financial stress!

Semi-Retirement

When you feel financially comfortable enough to slow down with traditional employment and maybe work 20-30 hours per week instead of the full grind of 40-50 hours, you are experiencing semi-retirement.

You can realize this stage by reducing your expenses enough where you don't need as much to live. Or perhaps you've developed enough passive (or happy active) income sources to cover your “needs” (housing, food, transportation, utilities) but you still want to do some work to cover the “wants”.

Having the ability to open up more of your week to relaxation and healthy living can do wonders for you and your family.

Here are some inspiring interviews I've done recently about “Semi-Retirement” movement:

- How Busy Moms Can Create a Successful Part-Time Business – with Crystalee Beck

- Creating a Flexible Work Schedule to Live Your Best Life Today – with Angela Rosmyn

- Slow FI and The Progressive Levels of Financial Independence – with Jessica from the Fioneers

Optional Work

Then there's the point when you have enough money from passive (or happy active) income sources to cover all your living expenses. Yes! This can be a reality, but as you can see, it takes time and many stages need to come before it.

These income sources can come from a variety of places. From the early retirement folks I've spoken to, they've fallen in the following areas:

- Stock dividends

- Taxable brokerage investment withdrawals

- Real estate investing

- Digital passive income (recurring revenue from affiliate income or advertising)

- Small businesses

Building up any of these 5 areas where you can live off them fully, can take decades of work. That's why if you want to get to the “Optional Work” stage, it helps to start early.

Decide Why You Want to Pursue Financial Independence

Like defining our financial independence plan, deciding why we want to be financially independent is quite personal as well. There can be a variety of reasons to consider a life of financial independence. Here are just a few:

Healthy Living

Perhaps you're working so many hours to pay for bills and a life you can't afford that it's taken an adverse effect on your physical and mental health. When you are in control of your money, you have the ability to structure your day in a way that promotes healthy living.

More Family Time

For some new parents, creating a financial independence plan can quickly become a necessity. Expectant fathers and mothers look for ways to spend more time with their children during their younger years. Getting our financial house in order is a great starting place. Personally, becoming a new Dad was one of my main drivers for financial independence.

Or maybe you want to spend more time with your parents as they grow older? We'll be glad that our financial independence plan was put in place years before.

Pursuing a Passion

For some of us, we pursued a career path that wasn't our true passion. And we look back 15 years later and asked ourselves, “Why am I doing this?”

If our financial situation is set up correctly, we can choose to pursue work we are interested in instead of work we have to do. This could be a small business, a different career path altogether (that maybe doesn't pay as much) or volunteer work that fills up our heart. And if we're lucky, perhaps this new passion gives you a healthier lifestyle and more family time as well.

Use the Right Tools to Implement Your Financial Independence Plan

It’s a lot easier to achieve your financial goals when you have the right tools. You can shave years off of your financial independence plan and countless hours of stress by simply preparing.

I’ve had the opportunity to interview over 200 personal finance experts, financially independent couples, and young millionaires on my podcast. Here are some of the tools that have helped them succeed with their big money goals.

Build and Live on a Budget

Tracking your personal cash flow with a budget has been the #1 response I receive from my podcast guests about how to win with money and achieve financial independence. If you don’t know what is happening with your money, your money will happen to you.

A lot of people know their income by heart, but not everyone knows what they spend each month. And that information can be more powerful when it comes to your financial independence plan.

Fortunately, tracking your expenses has become a whole lot easier recently. Here are 3 automated and convenient budgeting tools that can help you with your financial independence journey:

- Mint: Convenient app, part of the Intuit platform

- Tiller: Spreadsheet-based system (here's a tiller vs. mint comparison)

- Zeta: Designed specifically for couples (our full review of Zeta)

Track Your Net Worth

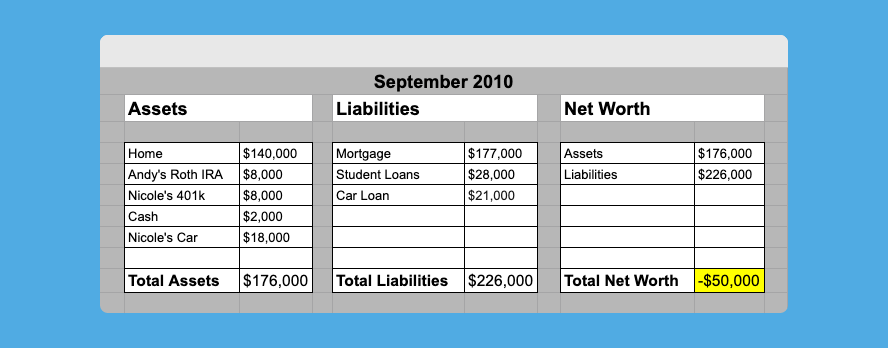

When my wife and I were in our late 20’s, we thought we were rich because we had a 6-figure income combined. Little did we know that our net worth was -$50,000 … and that was the true definition of our wealth. After that realization, we’ve been tracking our net worth ever since.

Your net worth is made up of your assets (all the stuff you own) minus your liabilities (all the stuff you owe). Some assets might include things like your home, investments, cash, and even your cars. Liabilities on the other hand include things like your credit card debt, student loans, and home mortgage.

Here's a snapshot of our net worth from 2010 when started tracking it (not so pretty):

If you want to improve your net worth, it’s important to track it. We’ve been using Personal Capital to track our net worth for the past few years and it’s helped us meet some of our big goals.

(FYI – the app is free, but they’ll want to work with you to invest your money. It’s not a requirement though. You don’t have to. I haven’t worked with them for investing.)

Automate Your Investments

Your net worth and wealth can start to truly grow when you invest your money. Compound interest is a magical and mathematical wonder as it helps your money make new money. In the case of saving for your retirement, that process can continue on for decades!

When you’re automatically investing each month through your 401k or Roth IRA, you’re making a commitment to your financial independence plan. After a while, you’ll forget you even had access to that money because you’ve gotten used to living without it.

As an example, I invested in my workplace 401k from 2014 through 2020 and maxed out my annual contributions. After 6 years and a generous 15% match from my employer, I walked away with a balance of almost $200,000!

Yes, the stock market surged upward substantially during that bull market time frame, but there were ups and downs. I left my investments alone and let automation do the work.

If you’re unsure of what to invest in for your workplace 401k or IRA, blooom is a partner that can help. For a small fee, a robo advisor service helps you with selecting the right funds and rebalancing your account. Automation and tools like blooom can give you the opportunity to relax and focus on other things in life besides the ups and downs of the stock market.

For more actual human professional help, consider a fee-only financial planner that is a “fiduciary” (someone who is out for your best interest, not theirs). Facet Wealth and XY Planning Network are two organizations to consider that adhere to that financial advising ethical code.

Final Thoughts on How to Create Your Financial Independence Plan

By defining our financial independence plan, deciding which path is right for us, and using the right tools, we will achieve our goals. It may not be a quick road, but it’ll be one that has purpose, direction, and clarity.

Throughout the entire process, we’ll need to grow the gap between our income and our expenses and invest the rest. This is the key to financial independence.

And when we reach our milestones, let’s be sure to celebrate them. We will have done something incredible for ourselves, our families, and for those we teach along the way.

What are you doing to create your financial independence plan?

Please let us know in the comments below.