When I read the Total Money Makeover by Dave Ramsey, I knew going through all of the 7 baby steps could take quite a while.

The book’s structure of saving money, paying off debt and investing was simple and easy to understand, but it definitely had some years attached to it. This was not a “get rich quick book” for sure.

Nevertheless, I was intrigued and inspired to follow all the way through Dave Ramsey’s Baby Step 7 and see where it took me and my new family.

10 years and two kids later, our family has become debt-free, mortgage-free, and millionaires. It is safe to say that this book was extremely beneficial to my family’s financial future.

I’m thankful to have found the book and the charismatic and inspiring author who wrote it.

But after the mortgage is paid off and we hit baby step 7 … What do we do then?

Baby Steps 8, 9 and 10

Instead of waiting for Dave Ramsey’s next new book to come out, I decided to create my next three baby steps. That would get me to the magic number 10.

The beauty of Dave Ramsey’s first 6 baby steps is they are very goal-oriented. Each step is specific and measurable. For example, Baby Step 1 instructs you to save $1,000 in an Emergency Fund. Baby Step 6 encourages you to completely pay off your mortgage. Very specific and easily measurable.

I’m going to try to use the same specificity and measurability with my made-up Baby Steps 8, 9 and 10.

Baby Step 8: Max Out Tax-Favored Retirement Accounts

“You must pay taxes. But there’s no law that says you gotta leave a tip.”–Morgan Stanley advertisement

Up until this point in Dave Ramsey’s Baby Steps, he’s told his readers to invest 15% of their income in tax favored retirement vehicles. In my humble opinion, Baby Step 8 is an excellent time to consider completely maxing those out to get their full benefits.

401k, 403b and 457 Plans

The annual contribution limits for a 401k, 403b and most 457 plans is $20,500 in 2022. If you have a fully-funded emergency fund and you’re completely debt free, it is time to max this baby out!

That being said, if your place of work has garbage investment options with low returns and high fees, this could be a whole different story.

At my previous place of work, we had index fund options with low fees. Additionally, my employer provided a 15% match on 100% of our contributions. So, if I invested $19,000 and the match was 15%, I got $2,850 additional that year.

Free money = awesome!

In a situation like mine, it makes complete sense to max out the 401k annually.

If your situation is not as favorable, talk with your workplace 401k plan manager about including some index funds and matching retirement benefits in the future. If you get an unfavorable response, no worries. Move on to maxing out the IRA.

Traditional IRA and Roth IRA

Let’s say we’ve maxed out our 401k plan because it has a favorable match and the investment options are solid. Now what?

Next up would be to contribute the maximum contribution level to a Traditional IRA or Roth IRA. Total allowed IRA annual contributions are $6,000 if you’re under 50 and $7,000 if you’re over 50.

With Traditional IRAs, you are eligible to receive a tax deduction when you make the initial contributions. Roth IRAs allow you to avoid paying the taxes when you withdraw your money because you paid those taxes from the start. Either option helps immensely in reducing your tax burden to Uncle Sam.

Given our situation, I moved on to fully fund my Roth IRA. We were under the income limits and I developed a solid portfolio that is generating excellent returns with low fees.

If you’re married, talk with your spouse about doing the same thing. This way, if you’re under 50, you’re contributing $12,000 per year into tax-favored accounts!

Health Savings Account (HSA)

Health Savings Accounts (HSAs) also have similar tax-favored benefits that are highly attractive. I didn’t have the option at my office, but I did sign up for mine through Lively.

These HSAs pack a triple tax benefit.

- You can contribute pre-tax (if you’re signed up for an HSA through your employer) or your contribution are tax-deductible if your employer doesn’t have an HSA option (like my previous employer).

- Funds inside an HSA grow tax-free!

- If you use the funds for qualified medical expenses, the funds can be withdrawn tax-free.

Down with you, taxes!!

Baby Step 9: Achieve Coast FIRE

When can I stop investing for retirement?

The answer is our Baby Step 9 which is called Coast FIRE!

Coast FIRE is when you have enough invested in your retirement accounts that you can decide to drastically slow down or completely stop new contributions and still retire comfortably in your 60s.

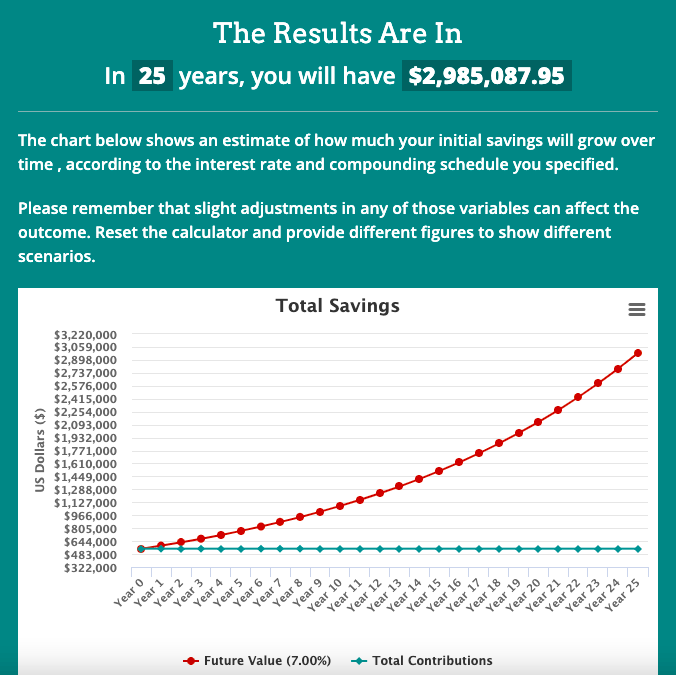

Our family hit Coast FIRE recently after saving up $550,000 in tax-advantaged retirement accounts before 40 years old. If our family simply did not add another dime to our $550,000, with a conservative 7% growth rate, we could expect to have around $3 million by the time we retire at 65.

Will we be stopping retirement contributions completely?

Not necessarily, but we’re sure glad we have the option to slow things down after saving and investing nearly 50% of our income for 10 years straight.

We will more than likely take advantage of employer 401k and HSA matches going forward but outside of that, we’re done investing for retirement.

What else can you do with the money then?

Well, there are two different pills you can take here …

- FIRE to YOLO: Relax and enjoy more life today with family and friends. Instead of hyper-saving and potentially dying with a pile of cash and investments, use more of your money to maximize your life experiences and create incredible memories with the ones you love.

- Baby Step 10: Continue building your legacy and wealth for generations to come. Your hard work and dedication can change the direction of your family tree as well as the causes you believe in most.

For the first pill, check out how our family went from 50% to 10% savings recently and why we’re happy saving less.

For pill #2, let’s move on to fake Baby Step 10!

Baby Step 10: Develop Your Passive Income

“Never depend on a single income. Make investment to create a second source.” – Warren Buffett

At this point, you’re debt-free, mortgage-free and you’ve hit Coast FIRE and hopefully still making a decent income. If you really want to accelerate things and go after some BIG dreams like a career change, early retirement, or an upgrade in your overall lifestyle, you’re going to need to increase your income.

If you’re like me and you don’t have a ton of extra time, passive income through buy-and-hold rental real estate or a taxable brokerage account can be a great way to go.

Perhaps time is on your side. Looking into a profitable small business can do wonders for your overall household income.

Rental Real Estate

This is a topic I’ve explored a lot.

Through some interviews on my weekly podcast, I’ve learned that you can get in the rental real estate game by getting a mortgage or buying with cash (Dave Ramsey's favorite).

If you go through the cash route, you’ll have to save for quite a while, but if you’re used to the Dave Ramsey “crockpot” methodology then waiting and saving shouldn’t affect you too much.

Once you’re able to secure your first property and those monthly rent checks start to come in, you’ll have a consistent and secure passive income source.

Yes, you’ll need to play landlord or hire a property management company to support you, but either way, you now have that coveted second income source that gets you closer to your big dreams.

If you don’t want to do the landlord thing, check out these options for investing in real estate the minimalist way.

Brokerage Account

Once you’ve exhausted your tax-favored accounts, you could look into a taxable brokerage account. I’m a big fan of Vanguard because of their transparency and ability to provide a boatload of low-cost investment options.

Additionally, M1 Finance has been showing up Vanguard lately with its low fees, auto rebalancing, and ability to buy slices of ETFs.

If early retirement is your game, you could consider an option like Target Date Funds. These investment options allow you to pick a specific year for your early retirement, invest consistently through dollar-cost averaging and “set it and forget it”. If you’re partnering with a low-cost brokerage partner like Vanguard, you’ll find these investment vehicles have decently low fees which allow you to retire earlier.

Alternatively, you can create and manage your own portfolio of diversified investments or work directly with a fee-only Certified Financial Planner. XY Planning Network has a load of professionals with a variety of specialties available to support you.

Small Business

Building your passion around a small business idea can be an excellent way to increase your joy and increase your income. I'm motivated by the hundreds of online business entrepreneurs I’ve spoken with who have developed a solid income by starting a blog, promoting their services and selling products.

Small business development does take time, patience and a whole lot of hard work to become successful. If you have spare time and the will to succeed, dip your toes in and see how the entrepreneurial water feels.

Last year, I decided to take this entrepreneurial leap full-time. I quit my job at 38 years old and decided to be a full-time online content creator. So far, I’m absolutely loving it!

There are definitely disadvantages of entrepreneurship (full-time), but there are plenty of advantages too.

The Final Destination: Bring In More Passive Income Than Your Expenses

“A wealthy person is simply someone who has learned to make money when they're not working.” – Robert Kiyosaki

We’re talking specific and measurable, right?

The final destination of all of these baby steps would be to generate enough passive income to completely cover your annual expenses.

This consistent passive income stream would allow you the freedom to change careers, retire early or dedicate more time to causes and hobbies that bring you the most joy.

Passive Income Example

Let’s say John is earning $60,000 at his full-time web developer job. He likes his career, but he isn’t positive his position is secure. The company, XYZ Interactive, has been going through some leadership changes recently. With the corporate shake-up, XYZ’s clients are leaving left and right.

Luckily for John, he has gone from Baby Step 1 all the way through Dave Ramsey’s Baby Step 7, AND he’s completed Baby Steps 8,9 and 10 as well. He’s built up enough passive income through his rental properties to net $36,000 annually. Since John is a big saver and squirrels away 50% of his income annually, his expenses are only $30,000.

His passive income of $36,000 exceeds his annual living expenses of $30,000! Ding, ding, ding! John wins the game of financial independence.

Essentially, John would be covered if there happened to be a “downsizing” at XYZ. If John didn’t get along with XYZ’s new management and he wanted to start his own web development firm, he would be well-positioned to do so.

John’s dedication to saving, staying out of debt and investing has provided him the ability to live his life on his terms.

Final Thoughts on Life After Dave Ramsey's Baby Step 7

Dave Ramsey's 7 Baby Steps create a fun, easy-to-follow way to conquer the mountain of financial independence, but it might not be for everyone. I've spoken to millionaire entrepreneurs who have built their businesses using debt or their real estate empire by leveraging properties. There's nothing wrong with that. Building a business with debt works for them and that method has brought them tons of financial success.

Personal finance is just that … it's personal. Not everyone's situation fits perfectly into 7 steps (or 10 for that matter).

Do what's best for you and your family. Your true contentment, personal satisfaction, and ability to follow your life's passion is the true measure of financial success in my book.

What would life look for you after Dave Ramsey's Baby Step 7? What do your Baby Steps 8, 9 and 10 look like?

Please let me know in the comments below.

23 Comments

Hey Andy,

Thanks for writing this (albeit a few years ago). My grand question once we all pay off our mortgages is so we leave all of our equity in the house just to let it earn a (measly) 3% appreciation? Couldn’t that money be better in a more favorable marketplace?

Also, when it comes to retirement and pulling your 4% annual, how do you withdraw from that equity?

Thanks,

Great questions! This all depends on your goals.

My goals may be different than yours.

In addition to growing my net worth, I’m interested in easing my financial burdens as well. Eliminating my mortgage did that for me.

Our home was grown in value from $350,000 to $450,000 in 7 years. Given that growth, it feels like a smart investment right now.

Not tapping the equity doesn’t bother me at this time.

If we want to buy another home in the future, we’ll be able to sell our appreciating asset (our home) to do that.

Thanks for a great article. It is being passed around our group that is focused on Baby Steps 6-7 and beyond, as we see need for support amongst those who ask, “What now?” However, I wish we could stop being babies at this point! What shall we call the next steps? Adulting steps 6-10? Leaps 6-10? Mature March 6-10? :-)

Ha! I love it! Adulting Steps is my favorite ;)

Congrats on making it to steps 8 – 10! That’s a huge accomplishment and you deserve to be able to pick whatever you want for those steps!

Thanks Derek! Personal finance is “personal”, right?! Do what’s best for you and your family and you’ll win.

I’d even argue that your Step 8 can/should go before Dave’s Step 7, because the investments will be returning more than today’s low mortgage rates.

For that matter, your #9 could come along anywhere in the journey. Developing multiple income streams makes the whole process easier and less risky than relying upon one source (day job paycheck).

Agreed! Getting those multiple streams of income cracking as soon as possible is a great recipe for success.

Way to expound on Dave’s Baby Steps! Being immersed in the church lifestyle myself, it was difficult for me to take away a ton of valuable information from the Dave Ramsey Course as I had no consumer debt, and I was worth about 100K when I went through his videos. I sort of started Wealth Well Done with with the vague vision of what to do with your life once you’ve completed Dave’s Baby Steps, which ultimately is aim for financial independence so you can launch your own ministries to fulfill your own purpose in life.

I really like the steps you offered here. They’re really financially based, like Dave’s are, but always remember, what wealthy people should ultimately be after is happiness, purpose, and contentness. Those are the true signs of a wealthy person, and the goal is to use our money to get to that blissful mindset and life.

Great job again, and I enjoyed reading your steps!!!!

You’re spot on! True wealth is personal contentment. Finding your passion and a place of service in the world will bring about the most financial peace. Best wishes on your mission my friend!

I love these, especially the passive income ones! I’m still working on that mortgage but there’s nothing that says you need to destroy that BEFORE earning more passive income! :)

Great list!

I completely agree. The sequential nature with regard to investing is not necessary in my opinion. When Dave asks people to stop investing while they are getting out of debt, I believe that limits the long term benefits of compound interest. He may have changed his stance lately – I’m not sure.

Passive income as early as possible in your life is an awesome concept! I’ll do my best to pass that information onto my kids so they can reach financial independence early in life.

I never even heard of DR until two years ago. Luckily, 40 years ago, when I got my first job I also started my first IRA. 5 years later I bought my first rental. The sequence of DR baby steps may work for many, but for me, investing early and often and letting others pay me has worked out just fine.

40 years of compound interest has definitely paid off for you! Whoever encouraged you to get your first IRA going back then deserves a thank you for sure. Congratulations on your success!

Great job! That is so awesome that you are about to complete the 7 steps! I am a big Dave fan; however, I must admit that I have favored investing over early mortgage retirement so I still have about 6 years on the mortgages. I noticed you said you don’t have an HSA at work. You should still be able to open one up at http://www.healthsavings.com as long as you have a high enough deductible on your health insurance plan.

God bless.

Mr. Bk2FI

You are smart to do that for sure! Dave has a lot of great advice but he definitely emphasizing crushing debt more than investing. I wish I would have started investing a lot more and a lot earlier.

Thanks for the HSA reference. I’ll check it out! I have a lot to learn there.

This is awesome, thanks you for sharing the “next steps”! Maybe 11, 12, 13 can include something along the lines of using your time to volunteer or give back to the community. I know Dave has the charity/giving back step, but it seems focused on monetary contributions (vs time once you are financially free and have the time to give!).

You are so right! We’ve been trying our best to both volunteer and (monetarily) give as a family throughout our financial journey but we can definitely improve in that area. We’re nowhere near donating 10% of our income as Dave recommends. We plan to increase our charitable giving each year as our net worth grows. As far as volunteer activities are concerned, I’m hopeful that when our kids get a little older, we can involve them more. Our local church has connected with great volunteer activities like reading to kids, becoming mentors and (of course) leading Financial Peace University courses.

Someone’s got to fill in those huge gaps from Dave Ramsey in the investing advice (lol). But seriously, great tips for getting finances together once you’ve achieved the basics.

Totally! Investing early and often isn’t emphasized enough. Compound interest is king.

Thanks for sharing! You hit all of them on the dot, so looks like you guys are on the right path! It’s impressive that you guys are almost done with your mortgage; that in and of itself is a tremendous accomplishment. I agree about the matching on the 401K’s (free money from employer), and other tax-advantaged spaces like IRA’s and HSA’s. Congrats on what you’ve accomplished thus far and good luck on your continued journey ahead!

Thanks so much Tim! We’re excited for what comes next in our journey. I hope it’s more time, freedom and fun with the family.